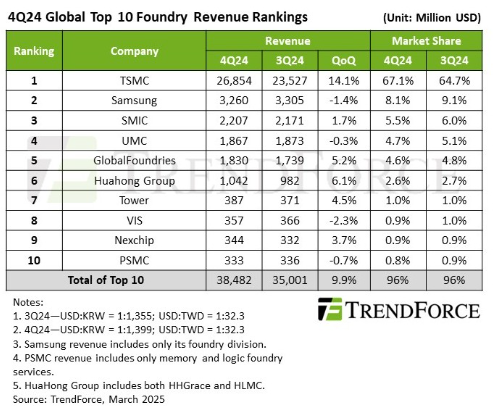

TrendForce reported that the top 10 semiconductor foundries estimated to have achieved nearly 10% QoQ revenue growth in 4th quarter of 2024, reaching US$38.48 billion. AI Server, PC processor and smartphone AP SoC have driven the growth while mature nodes revenues declined.

Other key findings by TrendForce:

TSMC saw QoQ growth in wafer shipments, which boosted revenue to $26.85 billion. The company secured a 67% market share to maintain its leading position. Samsung Foundry ranked second, with revenue declining 1.4% QoQ to $3.26 billion, representing an 8.1% market share. The revenue from new advanced-node customers could not fully compensate for the loss of orders from major existing clients, leading to a slight decline in sales.

SMIC faced customer inventory adjustments, resulting in a decline in wafer shipments. However, the ramp-up of new 12-inch capacity and an optimized product mix, which boosted blended ASPs, helped offset the losses. As a result, SMIC’s revenue increased 1.7% QoQ to $2.2 billion, securing a 5.5% market share and the third position.

UMC benefited from customers front-loading orders, keeping capacity utilization and shipments above expectations. This mitigated the impact of ASP declines, leading to a minor 0.3% QoQ revenue drop to $1.87 billion, ranking fourth. GlobalFoundries experienced increased wafer shipments and maintained fifth-place ranking. However, revenue growth was partially offset by slight ASP declines, resulting in 5.2% QoQ revenue growth to $1.83 billion.

HuaHong Group ranked sixth, with Q4 revenue increasing 6.1% QoQ to $1.04 billion. HHGrace’s 12-inch fabs saw slight capacity utilization improvements, boosting wafer shipments and ASPs. Meanwhile, HLMC benefited from China’s home appliance subsidy program and inventory replenishment, further increasing utilization rates.

Tower Semiconductor maintained its seventh-place ranking, with 4.5% QoQ revenue growth to $387 million, as ASP improvements offset the impact of lower fab utilization rates. VIS ranked eight, posting a 2.3% QoQ revenue decline to $357 million due to weaker consumer demand, though ASP growth partially offset shipment declines.

Among the top 10 foundries, Nexchip was the only company to shift rankings this quarter, moving up to ninth place with 3.7% QoQ revenue growth to $344 million. While it faced weaker demand for panel-related DDI, its CIS and PMIC shipments sustained its growth momentum. PSMC fell to tenth place, impacted by weaker demand for memory foundry and consumer-related chips. However, on a full-year basis, PSMC’s total revenue remained slightly higher than Nexchip’s.