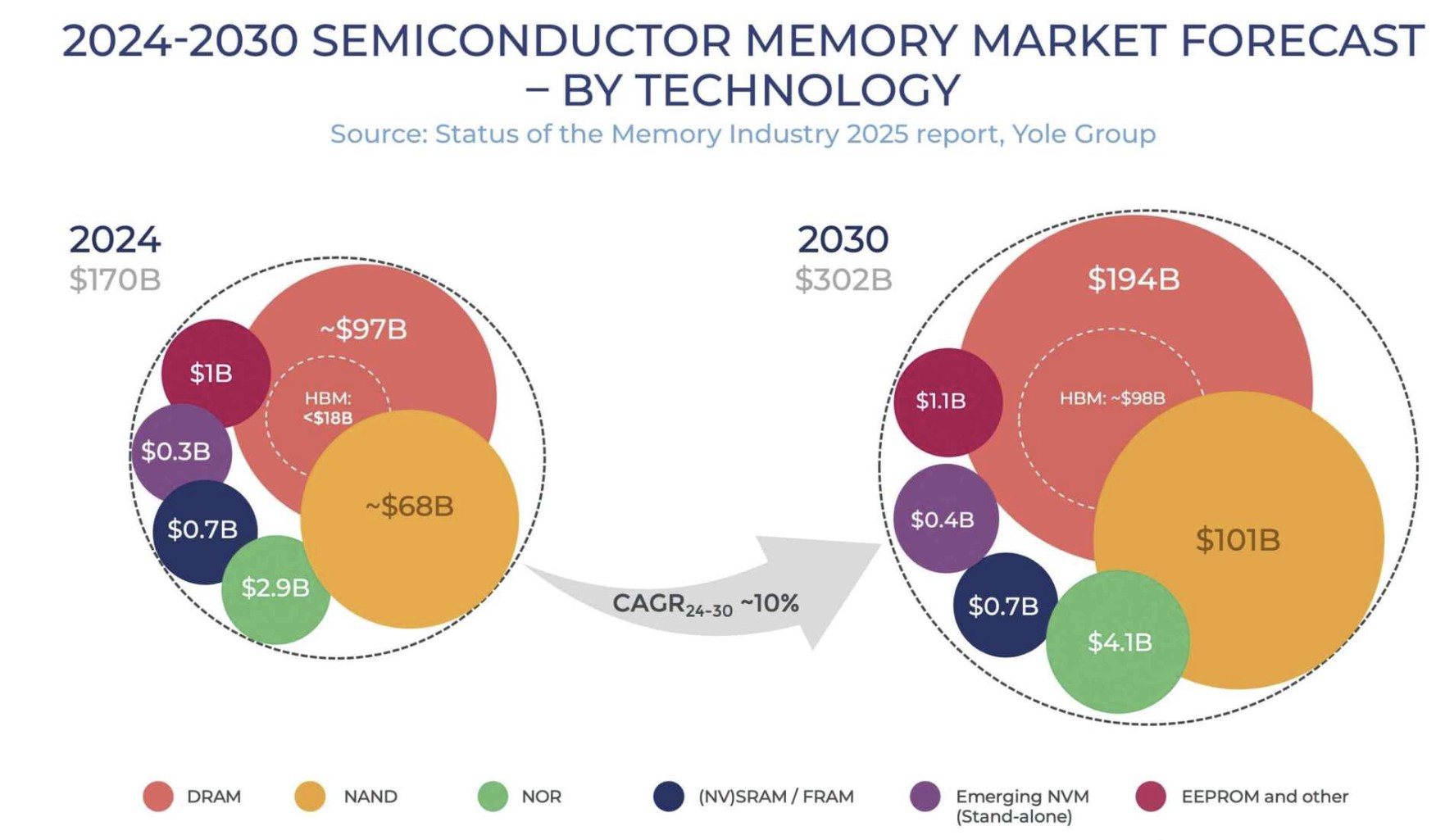

On June 19, 2025, Yole Group released its Status of the Memory Industry 2025 report, stating that global memory market revenue reached $170 billion in 2024, with DRAM at $97 billion and NAND at $68 billion. The report forecasts 2025 revenue to reach $200 billion, with DRAM projected at $129 billion and NAND at $65 billion. The growth is attributed to AI workloads and high-bandwidth memory (HBM), despite global trade tensions affecting supply chains.

In 2024, the memory market recovered from a 2022–2023 downturn, driven by AI training needs in data centers. HBM revenue is expected to nearly double to $34 billion in 2025, with a projected 33% CAGR through 2030, reaching $98 billion and exceeding 50% of the DRAM market. Conventional DRAM, including DDR, LPDDR, and GDDR, reached $80 billion in 2024 but is forecasted to grow at a 3% CAGR through 2030. NAND recovery was slower due to weak consumer demand and high inventory, leading suppliers to cut production to stabilize prices.

Trade tensions, particularly U.S. tariffs imposed in April 2025 targeting China, created supply chain uncertainty, prompting demand pull-forward in the first half of 2025. A 90-day tariff suspension provided temporary relief. NOR flash revenues also continued to recover in 2024.

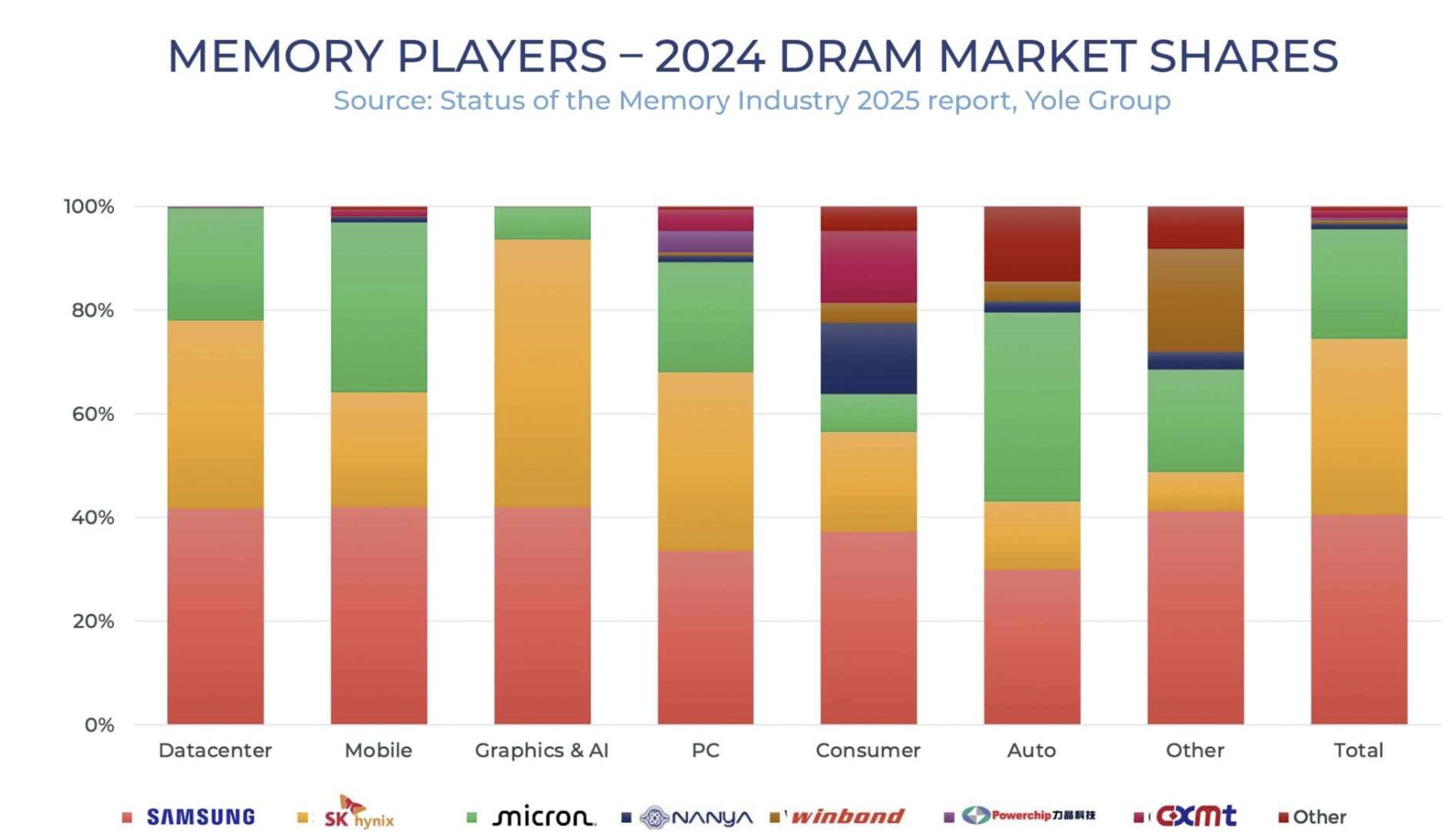

In the HBM market, SK hynix held a 54% share in 2024, supported by its Nvidia partnership. Samsung is advancing HBM3E validation with Nvidia, while Micron is increasing HBM3E production and established a Cloud Memory Business Unit. Chinese firms CXMT and YMTC intensified competition. CXMT disrupted DRAM with low-cost DDR3/DDR4, leading suppliers to shift to DDR5 and HBM. KingBank and Gloway launched China’s first DDR5 modules using CXMT’s G4 DRAM in 2024. YMTC introduced a fifth-generation 3D NAND chip with Xtacking 4.0 and a 294-layer architecture. Chinese companies are also investing in HBM amid export restrictions.

The report highlights AI as the primary growth driver, with shifts in supply chains and technology roadmaps reshaping the competitive landscape.