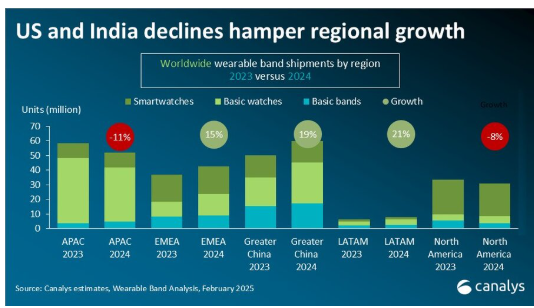

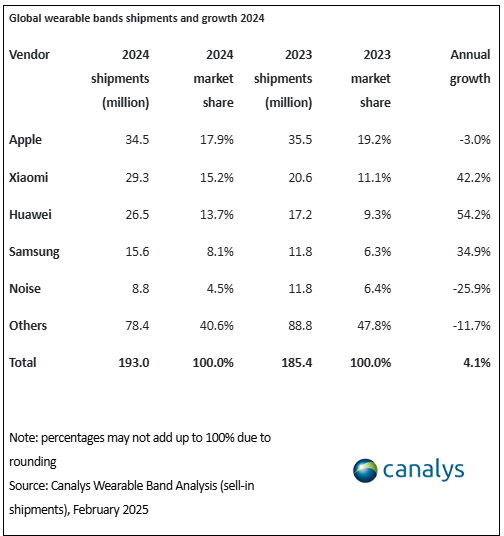

Canalys estimates global wearable band grew steadily in 2024 with total estimated shipments reaching 193 million units, up by 4% compared to 2023.

Further findings and analyst comments shared by Canalys:

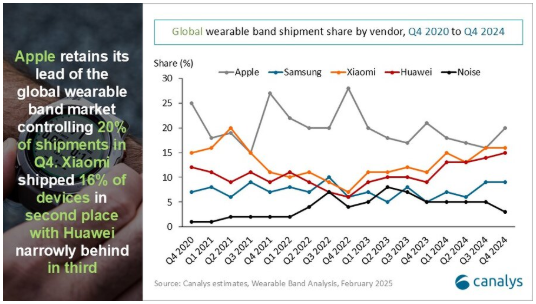

Growth was primarily fueled by strong demand in China and emerging markets, offsetting declines in mature regions, such as the US and India. The basic watch and basic band segments played key roles in driving entry-level adoption, while competition among the leading vendors intensified as Apple, Xiaomi and Huawei battled for market share.

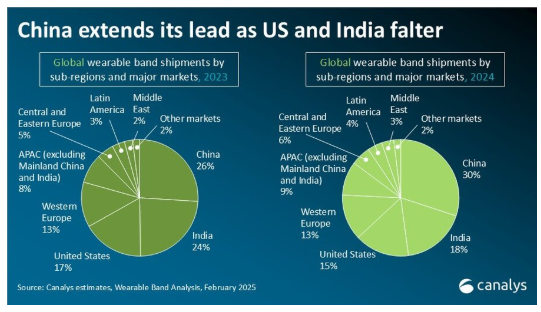

China remained the largest wearable band market, accounting for 30% of global shipments in 2024. It saw a strong 20% year-on-year increase, with Q4 alone growing 50% as vendors capitalized on a mix of government subsidies, product enhancements and strategic ecosystem integration.

“While China thrived, India and the US struggled, highlighting regional disparities in market performance,” said Canalys Research Analyst Jack Leathem. “India, the world’s second-largest wearable band market, saw shipments fall by 22% in 2024, as local vendors struggled to enhance functionality and performance in the basic watch segment, which accounted for 96% of India’s shipments.”

“Beyond China, emerging markets played a pivotal role in global growth, with Xiaomi, Huawei and TRANSSION building brand awareness and driving volume,” said Canalys Research Manager Cynthia Chen.

The Middle East led global expansion, growing 55% year on year, followed by Southeast Asia (45%), Latin America (21%) and Central and Eastern Europe (20%). Much of this growth came from affordable basic devices, as brands focused on price accessibility and retail expansion to capture first-time buyers.

The basic watch category remains a key driver of market growth, growing by 8% in 2024 following a strong 25% surge in 2023. Huawei and Xiaomi collectively held a 41% market share, with both companies actively diversifying their product portfolios. The evolution of basic watches is no longer limited to incremental upgrades of entry-level bands but is shifting toward more business-focused, advanced sports and medical-oriented devices, such as Xiaomi’s Watch S series and Huawei’s Watch D series.

Meanwhile, the basic band market has rebounded after years of decline. Shipments returned to growth in Q3 (up 7%) before accelerating sharply in Q4 (49%), driven primarily by Xiaomi (46%), Samsung (18%) and Huawei (17%). This resurgence highlights sustained consumer demand for simple, lightweight and non-intrusive wearables, particularly for health and fitness tracking. The rising popularity of smart rings suggests a growing preference for minimalistic wearable solutions.

Samsung’s re-entry into the basic fitness band segment with the Galaxy Fit 3 has filled a gap in its product lineup and intensified competition. This move has prompted Xiaomi to enhance its pricing and distribution strategies, particularly in Latin America, the Middle East and Southeast Asia, as part of its broader strategy to transition users to higher-margin wearables. Similarly, Samsung’s return to this category follows a strategic rationale: attracting new users to the Samsung Health ecosystem via entry-level wearables, then guiding them toward future smartwatch upgrades while expanding the ecosystem’s accessibility among budget-conscious and mid-tier Samsung smartphone users in these regions.

Outlook for year 2025:

Chen added that, “the wearable band market’s continued expansion in 2024 highlights the growing demand for affordable wearables in emerging markets. But mature markets face increasing challenges, with longer upgrade cycles and stagnant innovation slowing demand.”

“As vendors navigate these shifts, their success in 2025 and beyond will depend on balancing innovation with affordability, expanding their global reach and leveraging emerging trends, such as smart rings and advanced health tracking, to drive adoption,” said Leathem.

Source: Canalys