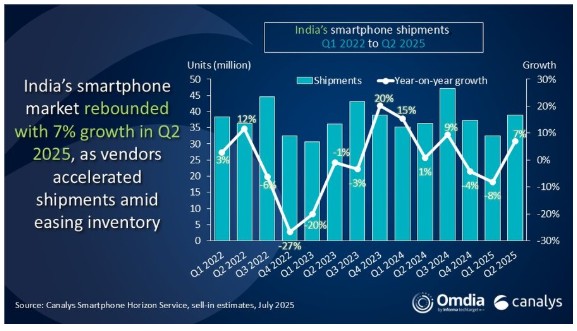

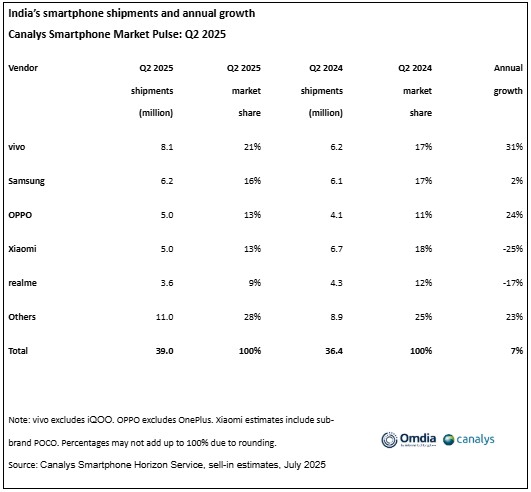

India’s smartphone market recorded a 7% year-on-year growth in Q2 2025, with shipments reaching 39.0 million units, according to Canalys (now part of Omdia). The rebound followed a slow Q1 marked by high inventory levels, with growth driven by new product launches and improved vendor activity despite challenges like extreme weather, US tariff tensions, and geopolitical uncertainty.

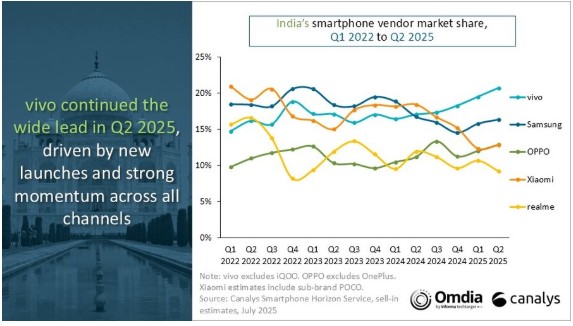

vivo led the market, shipping 8.1 million units and securing a 21% share, fueled by strong channel partnerships and the V50 series’ traction in Tier 1 and Tier 2 cities through large-format retail and wedding campaigns. The Y-series sustained demand in smaller cities, while the T-series grew online. Samsung held second place with 6.2 million units and a 16% share, leveraging financing schemes like 18- and 24-month zero-cost EMI for its A36 and A56 models. OPPO took third with 5 million units, driven by offline sales of the A5 series and online growth of the K13, narrowly surpassing Xiaomi, which also shipped 5 million units with momentum from the Redmi 14C 5G and A5, alongside a design-focused Note 14 series. realme rounded out the top five with 3.6 million units, balancing online softness with offline gains from the C73, C75, and 14X models, which accounted for 35% of its shipments.

Beyond the top five, competition intensified. Apple, ranking sixth, saw over 55% of its shipments from the iPhone 16 family, though the iPhone 16e faced post-launch challenges due to its single-camera design and limited Apple Intelligence features. Motorola, in seventh, expanded retail in smaller cities after urban growth. Infinix overtook TECNO as TRANSSION’s lead brand in India, contributing 45% of the group’s 1.8 million shipments with bold designs and campaigns targeting gaming and creator communities. Nothing surged 229% year on year, driven by the CMF Phone 2 Pro, Phone 3a, and Phone 3a Pro, appealing to young urban consumers.

Looking ahead to H2 2025, brands are focusing on channel execution over new launches, with incentive programs offering rewards like foreign trips and vehicles tied to Monsoon sales, Durga Puja, and Diwali. Retail upgrades, including better booth setups and stricter promoter targets, are accelerating, alongside expanded long-tenure financing for mid- to high-end models. Despite these efforts, Canalys projects a modest full-year decline for 2025 due to persistent structural demand challenges.