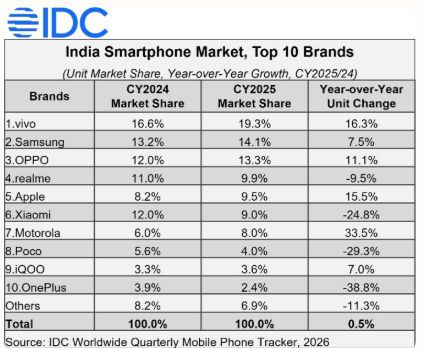

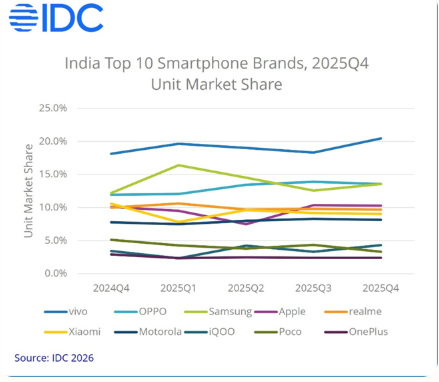

The International Data Corporation (IDC) reported that India's smartphone market recorded 152 million units shipped in 2025, a marginal year-over-year increase of 0.5%. Shipments started slowly in early 2025, rose in the second and third quarters, and fell 5% year-over-year to 34 million units in the fourth quarter due to post-festive inventory adjustments and cautious consumer spending.

Apple achieved record shipments of 14 million units in India in 2025, up 16% year-over-year, marking its fastest growth among its top five global markets. India ranked as Apple's fourth-largest market globally, behind the USA, China, and Japan. Apple held a 10% volume share overall and led by value with 29%. The iPhone 16 accounted for 4% of total smartphone shipments in India.

Average selling prices (ASPs) increased 8% year-over-year to a record US$282 in 2025, driven by higher component costs and demand for premium models. In the fourth quarter, ASPs rose 4% year-over-year to US$279, influenced by rising memory costs and rupee depreciation.

Segment performance in 2025 included:

Entry-level (sub-US$100): Shipments grew 18% year-over-year, share rose to 16% from 14%. Xiaomi and vivo led, with over 40% combined share. Motorola shipments increased nearly 2.4 times.

Mass-budget (US$100–US$200): Shipments declined 8% year-over-year, share fell to 41% from 44%. vivo, OPPO, and Motorola gained share; vivo T4X and OPPO A5 were top models.

Entry-premium (US$200–US$400): Shipments declined 5% year-over-year, share eased to 26% from 28%. vivo, Samsung, and Motorola grew; Motorola Edge 60 Fusion led shipments.

Mid-premium (US$400–US$600): Shipments expanded 23% year-over-year, share rose to 5% from 4%. Apple led, followed by Samsung and OPPO; key models included OPPO Reno 13 Pro, iPhone 13, and Samsung Galaxy A56/S24.

Premium (US$600–US$800): Shipments grew 37% year-over-year, share rose to 5% from 4%. Apple held 74% share with iPhone 16, iPhone 15, and iPhone 17 driving over 65% of shipments.

Super-premium (US$800+): Shipments grew 7% year-over-year, share steady at 7%. Apple led with 63% share; Samsung shipments rose 1.8 times to 34% share, led by iPhone 16 and Samsung Galaxy S24 Ultra/S25 Ultra.

Qualcomm-based smartphone shipments increased 23% year-over-year to 30% market share, driven by Xiaomi, POCO, OPPO, and Nothing devices. MediaTek's share fell to 46% from 54%, with shipments down 15% year-over-year.

The offline channel grew 12% year-over-year to its highest level in six years, expanding share to 57% from 51% in 2024. Online shipments declined 12% year-over-year, reducing share to 43% from 49%. Offline growth resulted from balanced omnichannel strategies, trade margins, and consistent pricing.

vivo maintained the top position in 2025 through diversified products and omnichannel execution, followed by Samsung (premium focus) and OPPO (strong offline presence). Xiaomi lost share, while realme, Motorola, and iQOO improved rankings. Nothing recorded the fastest brand growth at 45% year-over-year.

Market value grew 9% year-over-year in 2025 despite flat volumes, driven by premiumization. IDC expects shipments to decline in 2026 due to a global memory shortage, though premium demand and financing options may support value growth. Recent Android price increases suggest consolidation where scale becomes critical for supply and pricing management.

Aditya Rampal, Senior Research Analyst at IDC Asia Pacific, noted that fourth-quarter ASP increases from memory costs and currency factors reduced demand. Upasana Joshi, Senior Research Manager at IDC Asia Pacific, stated that scale and diversification were key success factors in 2025, with broad-channel vendors better positioned to maintain volumes.