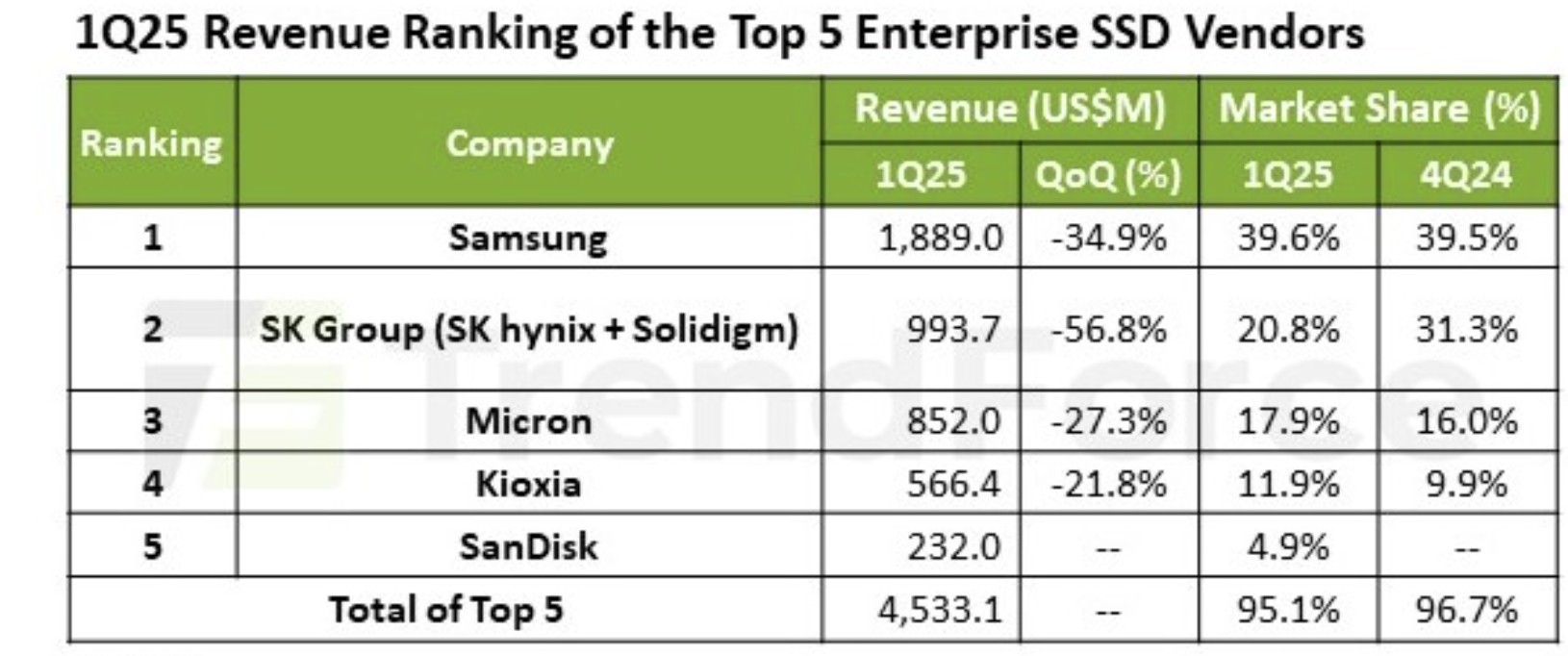

TrendForce reports that the enterprise SSD market experienced challenges in the first quarter of 2025 due to production issues for next-generation AI systems and ongoing inventory surplus in North America. These factors led major clients to reduce orders, resulting in a nearly 20% drop in the average selling price (ASP) of enterprise SSDs. Consequently, the top five enterprise SSD vendors saw quarter-on-quarter (QoQ) revenue declines.

Market conditions are expected to improve in the second quarter of 2025, driven by increased shipments of NVIDIA’s new chips and growing demand for AI infrastructure in North America. Additionally, Chinese cloud service providers (CSPs) are expanding data center storage capacity, contributing to projected revenue growth for the enterprise SSD market.

Samsung, the market leader, reported Q1 revenue of $1.89 billion, a 34.9% QoQ decline attributed to seasonal factors and reduced demand. However, its PCIe 5.0 product shipments increased, supporting market share growth in advanced interface technologies.

SK Group, comprising SK hynix and Solidigm, recorded Q1 revenue of $993 million, down over 50% QoQ, due to strategic order adjustments by key AI infrastructure clients. The company is advancing next-generation storage technologies, including PCIe 5.0 SSDs using TLC and QLC.

Micron’s Q1 revenue was $852 million, reflecting a 27.3% QoQ decline. The company saw continued demand for high-capacity shipments from 2024 and a gradual increase in PCIe 5.0 product adoption.

Kioxia reported Q1 revenue of $566 million, a 21.8% QoQ decrease, affected by seasonal demand weakness and lower orders from server OEM customers.

SanDisk achieved Q1 revenue of $232 million, with growth in product shipments. The company is focusing on high-capacity storage solutions, including SSDs with up to 1 petabyte of capacity.