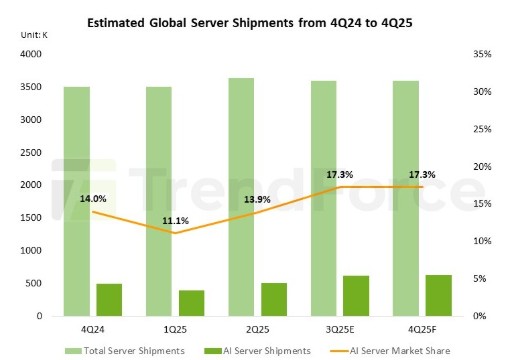

TrendForce reported that global AI server shipments are expected to increase by 24.3% year-over-year in 2025, driven primarily by demand from major North American cloud service providers (CSPs). Additional support comes from tier-2 data centers and sovereign cloud projects in the Middle East and Europe. However, geopolitical tensions and U.S. export restrictions affecting the Chinese market have prompted TrendForce to slightly adjust its forecast downward. Microsoft is prioritizing AI infrastructure investments, focusing on NVIDIA GPU-based solutions while its in-house Maia chips are not expected to scale until 2026. This focus has reduced its general-purpose server purchases.

Meta, meanwhile, has increased its general-purpose server demand, primarily using AMD platforms, to support new data centers. The company is also expanding its AI server infrastructure and expects to double shipments of its MTIA chips by 2026.Google’s server demand has grown due to sovereign cloud initiatives and new data centers in Southeast Asia. The company has begun mass deployment of its TPU v6e chips for AI inference in the first half of 2025. AWS is advancing its in-house AI strategy with the Trainium v2 platform and plans to start mass production of multiple Trainium v3 versions in 2026, expecting to double its self-developed ASIC shipments in 2025.

Oracle is focusing on AI server and in-memory database server purchases, planning to enhance its AI server infrastructure and integrate cloud database services with AI applications in 2025. The company is also seeing increased demand for NVIDIA’s GB Rack NVL72 solutions due to U.S. sovereign cloud projects. Server enterprise OEMs are reevaluating strategies for the second half of 2025 in response to changes in international tariff policies. TrendForce estimates total server shipments, including both general-purpose and AI servers, will grow by approximately 5% year-over-year, consistent with prior projections.