IC Insights: Semiconductor revenue for TVs to grow by 12% in 2014

The TV is no more passive broadcast receiver, it is turning smarter with a computing and digital networking capabilities. To connect seamlessly to a smart phone or a media server in-home and also to Internet, Smart TVs are integrated with additional electronics for computing and networking which requires more number of semiconductor ICs. To support high-definition digital-video, even the basic television circuit is using much larger and complex semiconductor content compared to traditional televisions. The leading semiconductor market researcher IC Insights has released its latest findings on the growing semiconductor content in TVs.

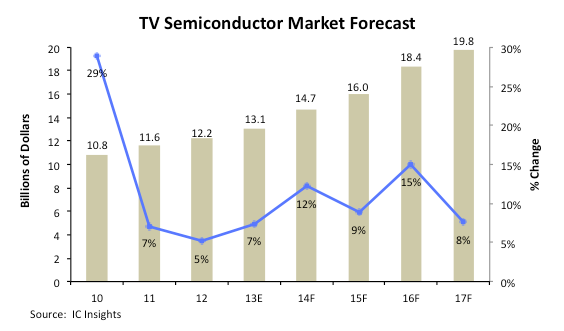

IC Insights has forecasted the semiconductor market for TVs to increase by an estimated 7% to $13.1 billion(See the figure below).

IC Insights says technologies such as wireless video connections, networking interfaces, multi-format decoders and LED backlighting have boosted the average semiconductor content in TV sets even as global TV unit shipments are forecast to decline by an estimated 3% in 2013. Further findings shared by IC Insights include: IC Insights projects that total global semiconductor revenue for televisions will grow 12% to $14.7 billion in 2014 due to an uptick in new TV sales in advance of the 2014 Winter Olympic Gam...

IC Insights says technologies such as wireless video connections, networking interfaces, multi-format decoders and LED backlighting have boosted the average semiconductor content in TV sets even as global TV unit shipments are forecast to decline by an estimated 3% in 2013. Further findings shared by IC Insights include: IC Insights projects that total global semiconductor revenue for televisions will grow 12% to $14.7 billion in 2014 due to an uptick in new TV sales in advance of the 2014 Winter Olympic Gam...

You've read this far — sign in to keep reading