Japan looses its hold on top semiconductor ranking

Date: 27/08/2013

In the electronics and semiconductor business, Japan holds a top position in many areas. But in the past two decades, its stronghold on the electronics and semiconductor industry is coming down. In semiconductor area, the companies from Japan occupy 4 to 5 positions in the top-10 ranking consistently for many years. If you look at the latest ranking by IC Insights for the first half of 2013, Toshiba is the only semiconductor company in the top 10 list. IC insights is provided the below insights on the subject of Japan's losing hold on top semiconductor ranking.

Anyone who has been involved in the semiconductor industry for a reasonable amount of time realizes this is a major shift and a big departure for a country that once was feared and revered when it came to its semiconductor manufacturing presence on the global market.

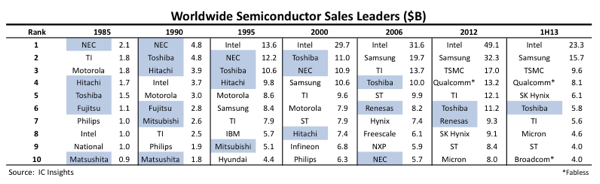

Figure 1 traces the top 10 semiconductor companies dating back to 1985, when Japanese semiconductor manufacturers wielded their influence on the global stage. That year, there were five Japanese companies ranked among the top 10 semiconductor suppliers. Then, in 1990, six Japanese companies were counted among the top 10 semiconductor suppliersa figure that has not been matched by any country or region since. The number of Japanese companies ranked in the top 10 in semiconductor sales slipped to four in 1995, then fell to three companies in 2000 and 2006, two companies in 2012, and then to only one company in the first half of 2013.

It is worth noting that Renesas (#11), Sony (#16), and Fujitsu (#22) were ranked among the top 25 semiconductor suppliers in 1H13, but Sony has been struggling to re-invent itself and Fujitsu has spent the first half of 2013 divesting most of its semiconductor operations.

Japans total presence and influence in the semiconductor marketplace has waned. Once-prominent Japanese names now gone from the top suppliers list include NEC, Hitachi, Mitsubishi, and Matsushita. Competitive pressures from South Korean IC suppliersespecially in the DRAM markethave certainly played a significant role in changing the look of the top 10. Samsung and SK Hynix emulated and perfected the Japanese manufacturing model over the years and cut deeply into sales and profits of Japanese semiconductor manufacturers, resulting in spin-offs, mergers, and acquisitions becoming more prevalent among Japanese suppliers.

1999 Hitachi and NEC merged their DRAM businesses to create Elpida Memory.

2000 Mitsubishi divested its DRAM business into Elpida Memory.

2003 Hitachi merged its remaining Semiconductor & IC Division with Mitsubishis System LSI Division to create Renesas Technology.

2003 Matsushita began emphasizing Panasonic as its main global brand name in 2003. Previously, hundreds of consolidated companies sold Matsushita products under the Panasonic, National, Quasar, Technics, and JVC brand names.

2007 To reduce losses, Sony cut semiconductor capital spending and announced its move to an asset-lite strategya major change in direction for its semiconductor business.

2010 NEC merged its remaining semiconductor operations with Renesas Technology to form Renesas Electronics.

2011 Sanyo Semiconductor was acquired by ON Semiconductor.

2013 Fujitsu and Panasonic agreed to consolidate the design and development functions of their system LSI businesses.

2013 Fujitsu sold its MCU and analog IC business to Spansion.

2013 Fujitsu sold its wireless semiconductor business to Intel.

2013 Elpida Memory was formally acquired by Micron.

2013 After failing to find a buyer, Renesas announced plans to close its 300mm and 125mm wafer-processing site in Tsuruoka, Japan, by the end of 2013. The facility makes system-LSI chips for Nintendo video game consoles and other consumer electronics.

2013 Unless it finds a buyer, Fujitsu plans to close its 300mm wafer fab in Mie.

Besides consolidation, another reason for Japans reduced presence among leading global semiconductor suppliers is that the vertically integrated business model that served Japanese companies so well for so many years is not nearly as effective in Japan today. Due to the closed nature of the vertically integrated business model, when Japanese electronic systems manufacturers lost marketshare to global competitors, they took Japanese semiconductor divisions down with them. As a result, Japanese semiconductor suppliers missed out on some major design win opportunities for their chips in many of the best-selling consumer, computer, and communications systems that are now driving semiconductor sales.

It is probably too strong to suggest that in the land of the rising sun, the sun set on semiconductor manufacturing. However, the global semiconductor landscape has changed dramatically from 25 years ago. For Japanese semiconductor companies that once prided themselves on their manufacturing might and discipline to practically disappear from the list of top semiconductor suppliers is evidence that competitive pressures are fierce and that as a country, perhaps Japan has not been as quick to adopt new methods to carry on and meet changing market needs.

It is not the strongest of the species that survive, nor the most intelligent, but the one most responsive to change. Darwin