Global cloud spending up by 21% in Q1 2024 to reach US$79.8 billion

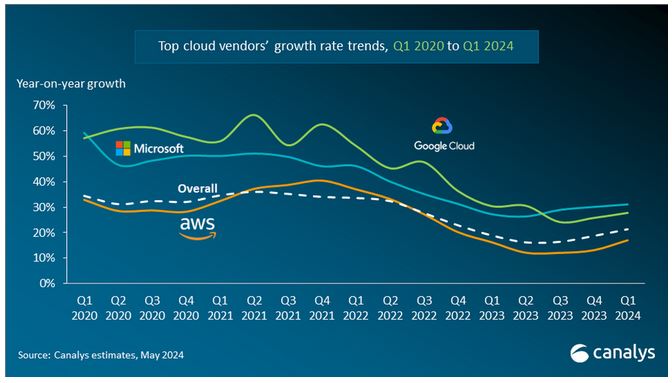

Market researcher Canalys reported that the worldwide cloud infrastructure services expenditure grew by 21% year-on-year in Q1 2024 to reach US$79.8 billion, an increase of US$13.4 billion. The top three cloud providers - AWS, Microsoft Azure and Google Cloud - collectively grew by 24%, accounting for 66% of total spending. All three hyperscalers experienced a growth rate surge, as enterprise cloud spending accelerated. However, Microsoft outpaced both AWS and Google Cloud, with sales rising by an impressive 31% year-on-year, nearly double AWS’s growth rate of 17%, while Google Cloud grew 28% year-on-year. Despite holding the largest market share, AWS faces increasing competition from its fast-growing competitors. In May 2024, the company announced the departure of CEO Adam Selipsky after three years in the role.

AI is an increasingly important demand driver of public cloud investment. The cloud effectively caters to the increased demand for computing and storage in AI applications. Global demand for AI integration with cloud technologies is motivating hyperscalers to integrate AI-enabled features into their cloud offerings and build strong partnerships with companies at the forefront of AI development. Enterprises are shifting their focus from optimizing cloud budgets toward i...

AI is an increasingly important demand driver of public cloud investment. The cloud effectively caters to the increased demand for computing and storage in AI applications. Global demand for AI integration with cloud technologies is motivating hyperscalers to integrate AI-enabled features into their cloud offerings and build strong partnerships with companies at the forefront of AI development. Enterprises are shifting their focus from optimizing cloud budgets toward i...

You've read this far — sign in to keep reading