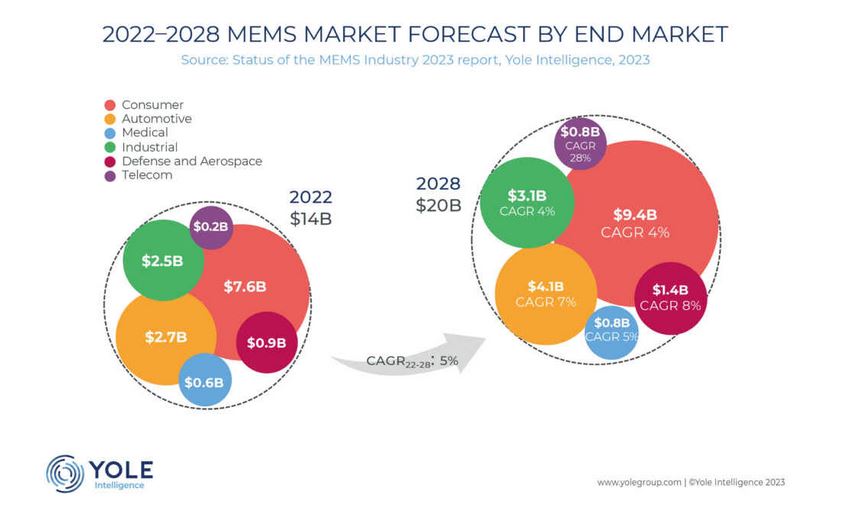

MEMS market to reach US$20 billion in 2028 at a 5% CAGR 23-28

MEMS devices are ubiquitously used in most of the latest electronics systems starting from simple consumer devices to aerospace defence electronics. Although there is a good demand for these components, there are a lot of suppliers in this market. Yole from its latest findings reported that MEMS market is set to grow from US$14.5 billion in 2022 to US$20 billion in 2028 at a 5% CAGR.

Below are the latest findings from Yole:

The consumer MEMS market remains the largest segment, where emerging wearable applications will offset the recent downturn in smartphone demand, growing from US$7.6 billion to US$9.4 billion at a 4% CAGR. The automotive sector continues to benefit from the increasing autonomous functionalities in cars and will remain the second largest market – while industrial, defense and aerospace, medical and telecom experiences CAGRs of at least 5% over the forecast period.

Pierre Delbos, Technology & Market Analyst, Yole Intelligence commented “With more than a billion of devices shipped worldwide annually, each containing numerous MEMS components, smartphones have typically been the main driver of the MEMS consumer market. However, as wearable technology matures and a greater number of end products are entering the market, they are beginning to take some of this market share...

Pierre Delbos, Technology & Market Analyst, Yole Intelligence commented “With more than a billion of devices shipped worldwide annually, each containing numerous MEMS components, smartphones have typically been the main driver of the MEMS consumer market. However, as wearable technology matures and a greater number of end products are entering the market, they are beginning to take some of this market share...

You've read this far — sign in to keep reading