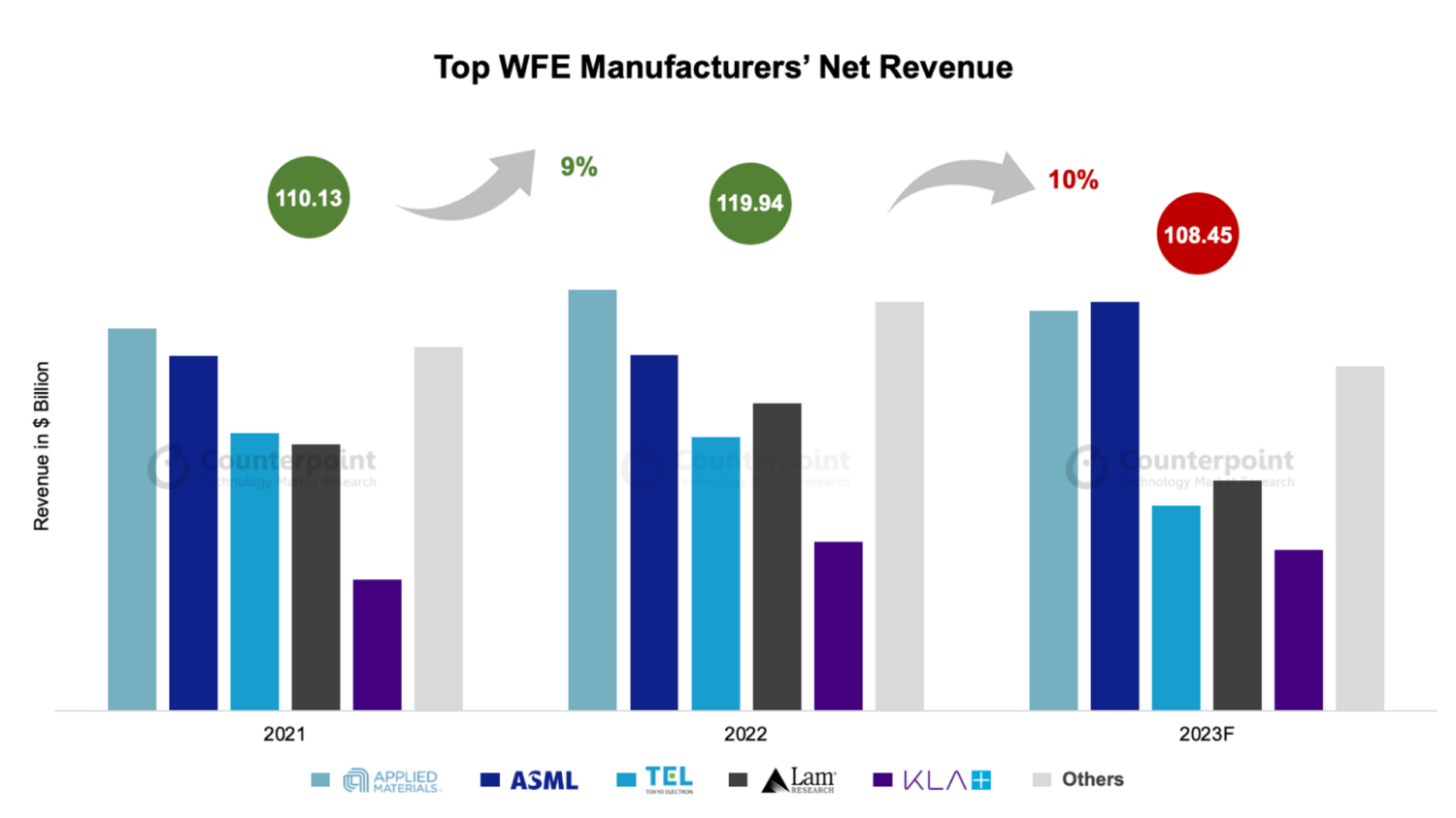

Semiconductor fab equipment revenues grew 9% to reach $120 Billion

Market researcher counterpoint has reported that the total semiconductor wafer fab equipment revenues from the manufacturers in this area grew 9% in 2022 to reach $120 billion. The top five manufacturers generated a revenue of $95 billion in 2022. However for the year 2023, the researcher forecasts a drop of 10% in revenue to reach US$ 108.45 billion.

Counterpoint said "The increase was due to continued strength in investments by customers for both leading and mature node devices across segments, including IoT, AI, HPC, automotive and 5G. The top five suppliers’ systems and service revenue increased to a record $95 billion." EUV lithography outlook remains strong due to the continued penetration of EUV into memory and logic, and foundries ramping up production of 3nm process nodes by applying Gate-All-Around transistor and FinFET architectures with increased EUV technology adoption, finds Counterpoint. Associate Director Dale Gai said, “During the past six months, TSMC has pushed out new capacities in 7/6nm and 5/4nm in the light of weaker market demand, while the capital spending on 3nm remains nearly the same as it planned at the beginning of 2023.” Commenting on the WFE market, Senior Analyst Ashwath Rao said, “The size of the WFE market in US dollar terms con...

Counterpoint said "The increase was due to continued strength in investments by customers for both leading and mature node devices across segments, including IoT, AI, HPC, automotive and 5G. The top five suppliers’ systems and service revenue increased to a record $95 billion." EUV lithography outlook remains strong due to the continued penetration of EUV into memory and logic, and foundries ramping up production of 3nm process nodes by applying Gate-All-Around transistor and FinFET architectures with increased EUV technology adoption, finds Counterpoint. Associate Director Dale Gai said, “During the past six months, TSMC has pushed out new capacities in 7/6nm and 5/4nm in the light of weaker market demand, while the capital spending on 3nm remains nearly the same as it planned at the beginning of 2023.” Commenting on the WFE market, Senior Analyst Ashwath Rao said, “The size of the WFE market in US dollar terms con...

You've read this far — sign in to keep reading