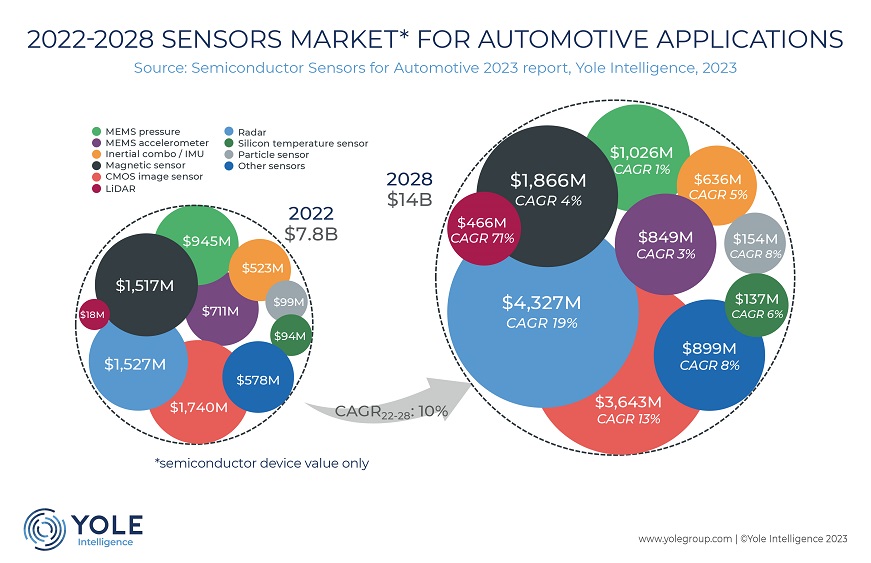

Semiconductor based automotive sensors to grow 10% CAGR 2022-28

Increasing count and usage of semiconductors in vehicles and their criticality in automotive market making them a priorty in automotive component' in auto-component supply chain management. Along with IC chips and discrete power semiconductor devices, semiconductor sensors becoming a key components in EV and ADAS enabled vehicles. Market researcher Yole finds automotive semiconductor sensor market to reach US$14 billion in 2028, with a 10% CAGR 22-28.

Below is the market size (US$s) of different semiconductor sensor components in 2022 as shared by Yole:

CMOS image sensors: 1740 Millions

Radar Sensors: 1527 Millions

Magnetic sensors: 1517 Millions

mems pressure sensors: 945 Millions

mems accelerometer sensors: 711 Millions

Inertial combo/IMU: 523 Million

Semiconductor temperature sensor: 94 Million

Particle sensor: 99 Million

Lidar: 18 Millions

Others: 578 Million

The top growth is estimated by Yole in: Lidar to grow by 71%, Radar by 19% and CMOS image sensor by 13% by 2028.

Though semiconductor sensors find use in every part of the vehicle. Major drivers of market are electrification of vehicles, ADAS, safety-related systems. Among the automotives, cars are the biggest market. Along with powertrain ADAS & Safety, the User Experience domain will witn...

Though semiconductor sensors find use in every part of the vehicle. Major drivers of market are electrification of vehicles, ADAS, safety-related systems. Among the automotives, cars are the biggest market. Along with powertrain ADAS & Safety, the User Experience domain will witn...

You've read this far — sign in to keep reading