The top capex spenders in semicon industry for 2014, forecast by IC Insights

IC Insights has release its forecast ranking of the top 25 semiconductor capital spenders for 2014. A preview of the top 10 spenders is shown in Figure 1.

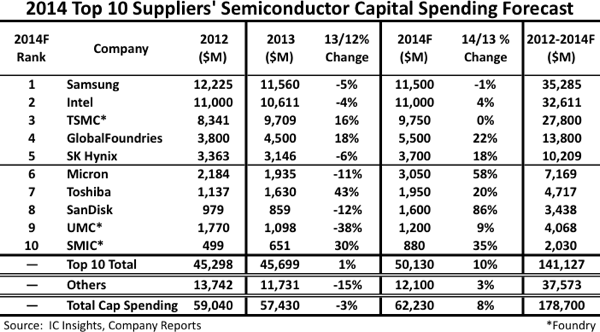

Fig 1 Below are other details shared by IC Insights: Samsung and Intel are each forecast to spend at least $11.0 billion this year, and TSMC slightly less than $10.0 billion. Collectively the three companies are forecast to account for 51.8% of total semiconductor industry capex this year. As amazing as that number is, it is a decrease from the 55.5% share these three companies held in 2013. Among the top 10, six companies are forecast to spend at least $3.0 billion in 2014, and nine suppliers are forecast to spend more than $1.0 billion. After keeping their combined spending essentially flat in 2013, the top 10 spenders are forecast to boost capex spending by 10% in 2014. After chopping its capital spending by 28% in 2012 and 12% in 2013, SanDisk is forecast to show the largest capital spending percentage increase (86%) among the top 10. The company stated that this large increase is needed to expand production of advanced 3D NAND flash memory with its manufacturing partner Toshiba. While SanDisk’s capital spending level is expected to be much higher than in 2013, this increased spending is not expected...

Fig 1 Below are other details shared by IC Insights: Samsung and Intel are each forecast to spend at least $11.0 billion this year, and TSMC slightly less than $10.0 billion. Collectively the three companies are forecast to account for 51.8% of total semiconductor industry capex this year. As amazing as that number is, it is a decrease from the 55.5% share these three companies held in 2013. Among the top 10, six companies are forecast to spend at least $3.0 billion in 2014, and nine suppliers are forecast to spend more than $1.0 billion. After keeping their combined spending essentially flat in 2013, the top 10 spenders are forecast to boost capex spending by 10% in 2014. After chopping its capital spending by 28% in 2012 and 12% in 2013, SanDisk is forecast to show the largest capital spending percentage increase (86%) among the top 10. The company stated that this large increase is needed to expand production of advanced 3D NAND flash memory with its manufacturing partner Toshiba. While SanDisk’s capital spending level is expected to be much higher than in 2013, this increased spending is not expected...

You've read this far — sign in to keep reading