US contributed hugely for the growth of fabless semiconductor biz

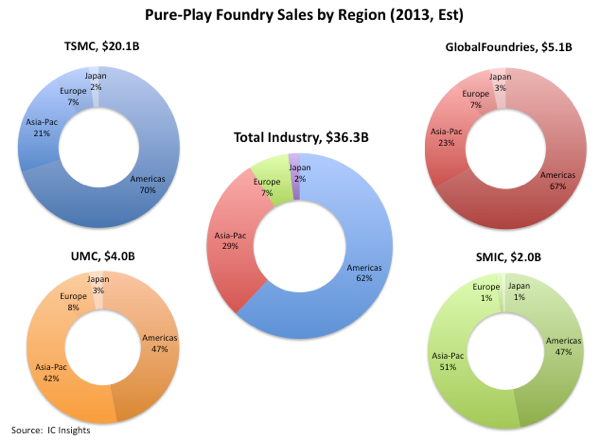

When it comes to semiconductor technology space, United States holds the leading position in multiple areas. US has most advanced semiconductor fabs in the world and also the best fables semiconductor companies in the world. As for the latest study by IC insights, customers in the Americas region (primarily the U.S.) are expected to account for nearly two-thirds of pure-play foundry sales in 2013, a slight increase from 2012. IC Insights forecasts that Americas region will represent 70% of TSMC’s sales, 67% of sales from GlobalFoundries, and 47% of sales from both UMC and SMIC, see the figure below.

While the revenue of fabless design companies grow in US, China and Taiwan emerging as the next region in growth of revenue and number of fabless chip companies. Below is the analysis shared by IC insights on this subject: The Americas region is forecast to account for $22.4 billion of the $36.3 billion worldwide pure-play foundry market in 2013, which is up from $19.2 billion (61%) of the total $31.7 billion pure-play foundry market in 2012. The Asia-Pacific region is forecast to represent $10.7 billion (29%) of pure-play foundry sales in 2013; and Europe, $2.5 billion (7%). Japan is by far the smallest market for pure-play foundry sales and is forecast to hold only a 2%...

While the revenue of fabless design companies grow in US, China and Taiwan emerging as the next region in growth of revenue and number of fabless chip companies. Below is the analysis shared by IC insights on this subject: The Americas region is forecast to account for $22.4 billion of the $36.3 billion worldwide pure-play foundry market in 2013, which is up from $19.2 billion (61%) of the total $31.7 billion pure-play foundry market in 2012. The Asia-Pacific region is forecast to represent $10.7 billion (29%) of pure-play foundry sales in 2013; and Europe, $2.5 billion (7%). Japan is by far the smallest market for pure-play foundry sales and is forecast to hold only a 2%...

You've read this far — sign in to keep reading